When a homeowner dies, dealing with legal and financial complications can be tough. This is particularly true for mortgage payments. Many people forget to think about mortgage rules during the estate planning process. This article will explain what happens to a mortgage when someone passes away. It will offer helpful information for the surviving spouse and family members.

Understanding Mortgage Obligations After Death

When a person dies, their financial debts, like home loan mortgage debt, don’t go away. The mortgage loan is still connected to the home, and creditors can pursue the collection of these debts. If payments are not made, the lender can take the house back, even if the homeowner has died. This can make things harder for family members who are already dealing with their loss.

It’s key to know that the mortgage lender can take back their money if needed. However, heirs or beneficiaries have several options. This article will explain these choices. They can either take over the current mortgage or sell the house. Each option will impact their finances in different ways.

What happens to mortgage debt?

When a person dies and has a mortgage, their estate must pay this debt. The estate includes the things owned and the debts of the deceased person. It is in charge of paying off any leftover debts, including the mortgage.

If the estate has enough money, the mortgage can be paid. This will not affect the heirs. But if there isn’t enough money, the executor of the estate might need to sell some things. This could mean selling the property with a mortgage to pay off the debt.

It is important to know how to deal with mortgage debt when someone passes away. Talking to an estate planning lawyer can show you the right steps to take in your state. This can help make things easier and protect your loved one’s legacy.

Legal responsibilities of heirs and co-signers

Understanding what happens to a mortgage after someone dies is important for heirs and co-signers. Estate planning should cover these situations. This can help ease stress for family members.

If someone like a spouse or family member signs the mortgage with you, they need to take care of the loan too. This means they have to keep making the mortgage payments.

If the dead person was the only one who borrowed, the estate had to pay the debt. When the property goes to the heirs, the mortgage lender will talk to them according to state law and federal rules.

Navigating Mortgage Payments and Property Inheritance

Dealing with losing someone you love is hard. It can feel even tougher if you get a property that has a mortgage. Knowing your options may help lessen some stress during this tough time.

Deciding what to do with your property can be tough. You have several choices. You can keep it, manage the mortgage, sell the house, or explore other options. Your choice will depend on different factors. These factors include your financial situation and your personal goals.

Options for inheriting the property

When you buy a property with a mortgage, you have different choices. Each choice can help with different money needs and goals.

You can take over the existing mortgage first. This means you can keep the same terms. There is no need to apply for a new loan. However, you must show the lender that you can afford the payments.

Another option is to sell your property. You can take the money you earn from selling to pay off the mortgage. This is a good choice if you cannot afford the mortgage payments. Here’s a list of your options:

- Assuming the mortgage: You can hold on to the property and continue paying the same mortgage payments.

- Refinancing the mortgage: You can find a new loan that may offer better rates or terms.

- Selling the property: You can sell the property, use the money from the sale to pay off the mortgage and divide any extra money with the beneficiaries.

- Deferring payments: You can temporarily pause payments while you look for better long-term choices.

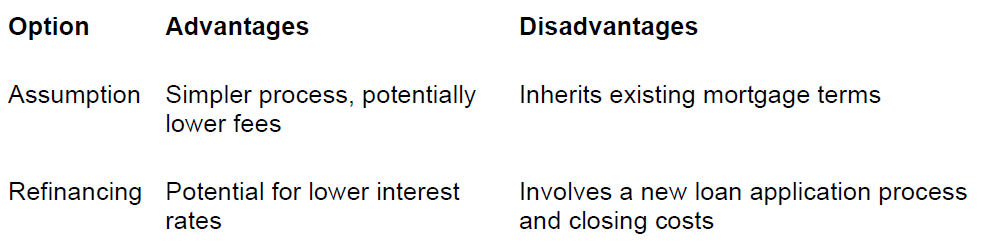

Assumption vs. Refinancing: What You Need to Know

When you have an inherited property with a mortgage, you typically have two main choices: assumption and refinancing. Each choice has its benefits and drawbacks. What works best will depend on your financial situation and what you want to achieve.

Assumption means you accept the current mortgage with its conditions and rules. This method is often simpler. It requires less paperwork and usually has lower fees. However, the existing mortgage rate might not be as good as the rates available today.

Refinancing is when you get a new loan to replace your current mortgage. This might help you get a lower interest rate. You can also change your loan terms or use your home equity. The best choice for you depends on your personal situation.

Carefully considering both options is very important. Talking to a money expert can really help. This way, you can make a smart decision that matches your financial goals.

Dealing with Mortgage Companies Post-Mortem

After someone you love passes away, it is very important to handle their financial issues. This is especially true for mortgage companies. Informing them quickly can help things run smoothly. It can also stop problems like late fees or foreclosure.

- Tell the mortgage company about the death.

- Send them a copy of the death certificate as soon as you can.

- You might need to keep making payments based on the loan terms and state laws.

- This may be true while probate is going on or before the ownership of the property changes.

- If there is a will, sending a copy can help show who owns the property.

- Your credit score will not change just because of the death.

- However, if you co-signed the loan, not managing the financial tasks correctly could hurt your credit score.

Steps to notify mortgage companies

When a loved one dies, it’s important to first handle urgent matters. After that, you should let their mortgage company know. Doing this quickly can stop problems like missed payments. It also helps keep the credit history of the deceased safe.

Start by getting the documents you need. You will need the death certificate and mortgage account information. After you have these, call the mortgage company to let them know what happened. Show them a copy of the death certificate. Then, ask what steps you should take next.

Mortgage companies might ask for more papers, like a will or documents from the probate court. They need these to check who the executor is and who the beneficiaries are. They will help you know what to do next regarding the deed. This could mean taking on a loan, making changes to it, or looking at other options based on your situation.

Documentation required for notification

When you need to inform a mortgage company of death about a deceased person’s name and the borrower’s death, it’s key to have the correct documents ready. This will help make the process easier for everyone involved. Having these documents shows you are being honest and helps you communicate clearly. It also helps the mortgage company understand the situation faster.

You need some important documents. These are the death certificate, the mortgage statement, or the loan account number. A government-issued photo ID is also required. You may need to provide proof of your relationship to the person who died. This could be a will or papers from the probate court.

If mortgage protection insurance (MPI) is part of your estate planning, share the policy details related to the loan balance. This helps speed up the claim process and makes sure the mortgage gets paid. Keeping these papers ready when you contact the mortgage company after death will make the situation easier. This can help avoid delays or problems.

Conflict Resolution Among Multiple Heirs

Inheriting property can cause issues in families, especially when there are many heirs. If they can’t agree on selling the property or managing the mortgage and sharing ownership, it can add stress. This can make the situation much tougher for everyone involved.

To solve these problems, you can look for a mediator or hire an estate lawyer. They can assist with communication and address any concerns. They will also help ensure fair choices, which can reduce possible conflicts.

Understanding rights and obligations

When several heirs own a property with a mortgage, they should understand their rights and responsibilities. This knowledge can help avoid problems and confusion that arise from not knowing what to expect.

- Keep talking with each other.

- Heirs need to say what they want to do.

- They might want to keep the property, sell it, or buy their siblings’ parts.

- It’s smart to talk with an estate planning lawyer.

- This will help everyone know their legal rights.

Decisions about inherited property should involve everyone. All heirs must agree on the choices. It is important to think about each heir’s financial situation, their link to the property, and their plans for the future.

Strategies for equitable distribution

Dividing a property that one inherits and has a mortgage takes careful thought, especially regarding the remaining mortgage balance and any potential due-on-sale clause. You need to be fair to all the heirs. It is important to look at each heir’s financial situation. You should also think about what they want and their goals for the future. This can help prevent any disputes.

If the estate plan does not explain what to do with the property, there are some options. The heirs can sell the house and split the money. One heir can take over the mortgage and pay the others. They could also choose to share ownership of the property.

Co-owning a property needs a clear agreement. This agreement must say who will pay the mortgage payments and property taxes. It should also explain how to handle maintenance and any future sales. Good communication matters a lot. If everyone is willing to compromise, it can lead to a better result.

Conclusion

Dealing with mortgage payments after losing a loved one can be tough. It is important to know what heirs and co-signers should do to get through this situation. If you want to take over the loan or refinance, understanding your options is important. You should talk to mortgage companies right away and send any needed papers. If there are several heirs, it is crucial to learn everyone’s rights and duties to make sure things are fair. Getting help from experts can also guide you during this hard time. If you have more questions or need support, please contact us.

Frequently Asked Questions

Can mortgage payments be deferred after the owner’s death?

If you can pause mortgage payments after someone passes away depends on the loan servicer and state law. A surviving spouse or heir may ask for a short break in the

payments. It is important to call the loan servicer quickly to talk about options and avoid penalties.

What should heirs do if the deceased did not leave a will?

If there is no will, the court will appoint an executor to manage the estate. The executor must handle the mortgage payments using the estate’s assets or decide on selling the property to settle the debt.

Important Disclosures:

This information is not intended to be a substitute for individualized legal advice. Please consult your legal advisor regarding your specific situation. This material was prepared by Midstream Marketing.