Retirement is a big change in your life. Planning is key to feeling safe with your money during this time. A good retirement budget can make you feel calm. It helps you enjoy your golden years without worrying about cash all the time. A strong nest egg and consistent retirement income are important for your financial safety after you retire. Let’s look at the main steps to make a full retirement budget.

Understanding Retirement Financial Security

Retirement financial security means having enough money to pay for your living expenses once you stop working. It’s not just about having a lot of money all at once. What’s more important is creating a steady income during retirement. This way, you can live how you want.

Social Security benefits are important for retirement income for many people. However, depending only on these benefits may not give you enough money. It is important to know your expenses and the income you can get. By understanding this, you can figure out how much money you need to save and how to handle your money well during retirement.

The Role of Budgeting in Achieving Financial Peace

A retirement budget is similar to a map. It shows you where your money comes from and helps you decide how to spend it. This budget helps you save money for important needs and enjoyable activities. It also ensures that you do not run low on savings.

Having a retirement budget is a smart choice, no matter if you want a lavish retirement or a simple one. Tracking your income and expenses will help you handle your money better. A budget can stop you from running out of funds and can give you peace of mind. You will clearly see your annual income and expenses. This makes it easier to change things if needed and to stay within your limits.

Cash Flow Considerations for Planning Your Future

Having enough money coming in is important for a comfy retirement. Once you no longer get a steady paycheck, you will depend on your savings, investments, and other income to pay for retirement expenses.

- Check your income and expenses often.

- Look at your savings and investments regularly.

- Ensure you have enough for your daily needs.

- Plan for any surprise costs that may come up.

- Think about how long your money will last.

- Review your financial goals and change them if needed.

- Remember to include any pensions or benefits.

- Stay updated about changes in taxes or rules.

- Estimating retirement expenses: Consider how your costs could change. This includes things like healthcare, travel, or new hobbies.

- Social Security payments: Check if you can get Social Security. See how much you might receive each month.

- Cost of health care: Keep in mind that healthcare costs may go up as you get older. Make sure to include health insurance costs.

- Other income sources: Look at any money you might earn from pensions, rental properties, or part-time jobs.

Crafting Your Retirement Budget

Creating a practical retirement budget is about you. It depends on your life, habits, and money goals. First, write down all the sources of income you think you will have. Next, estimate how much money you expect to get from each source of income.

After that, make a list of all your retirement costs. It’s important to divide them into two parts: essential expenses and discretionary expenses. This way, you can adjust your spending if you need to.

Identifying Fixed vs. Variable Expenses

When you create your retirement budget, it is important to know about fixed and variable expenses. Fixed expenses stay pretty much the same over time. They include costs like housing payments, property taxes, and insurance premiums.

Variable expenses can change from month to month. They include costs like groceries, utilities, and transportation. These expenses also cover discretionary expenses, such as entertainment and eating out.

Knowing your average monthly expenses can help you guess future costs. You can’t change fixed expenses a lot, but you can cut down on variable costs. This helps you manage your budget better.

Adjusting Your Budget for Retirement Lifestyle Changes

Retirement brings new and fun changes. You can enjoy your hobbies and interests freely. But, it’s smart to think about how these changes can impact your retirement budget. Doing things like traveling, trying out new hobbies, or spending more time with family can all change how you spend your money.

If you want to travel a lot during your retirement years, you should save money specifically for travel expenses. Also, if you have a hobby that you enjoy, don’t forget to add its costs into your budget.

Thinking about changes to your lifestyle for retirement can help you create a better plan. Your retirement budget should be easy to adjust. It should change as your needs and wishes change over time.

Strategies to Maximize Your Retirement Savings

Saving regularly as you work is important for building a good nest egg. Try to add more money to retirement accounts, such as 401(k)s and IRAs. By doing this, you can gain from compounding returns.

- Think about different ways to invest.

- You can try real estate or stocks that give dividends.

- These can help grow your retirement income.

- Also, remember to check your investment portfolio often.

- This way, you can keep it matched with your risk tolerance and financial goals.

Tips for Efficiently Managing Retirement Accounts

Managing your retirement accounts is very important. It helps your money grow so you have enough savings for your retirement years. You should check your portfolio often. Make adjustments to keep the right balance of assets. This balance depends on how much risk you can take and how long you want to invest.

Consider asking a certified financial advisor for help. They can show you how to invest your money wisely. You might also want to look into target-date funds or annuities. Using tax-friendly retirement accounts, like Traditional or Roth IRAs, may simplify your taxes. Keep in mind that websites like Vanguard offer many investment choices and tools to help you make smart decisions for your retirement savings.

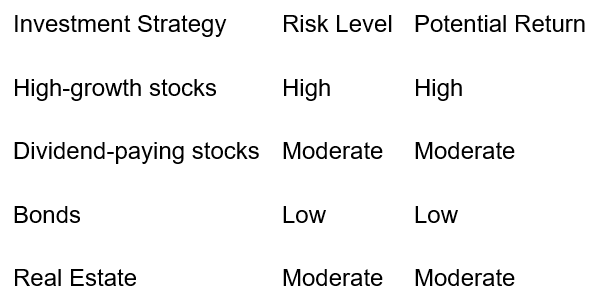

Investment Strategies for Sustainable Income

Generating regular income from your nest egg is important for a good retirement. You should consider diversifying your investments. Put your money into different places like stocks, bonds, and real estate. This can help reduce your risk and may also increase your earnings.

- Look at low-cost index funds or exchange-traded funds (ETFs).

- These options may help you access many markets and save on taxes.

- Consider if an annuity fits into your retirement income plan.

Having a good retirement income plan is very important. This plan should mix ways to grow your money and make income. It makes sure your savings keep working for you while you enjoy your retirement.

Ensuring a Steady Retirement Income

Having a steady income when you retire gives you financial security. This helps you enjoy your retirement years without worrying about money. A lot of people rely on Social Security benefits for a big part of their retirement income. However, this money is often not enough to pay all their bills.

To fill this gap, you can find other ways to make money. Some options include pensions, investments, or part-time jobs. By doing these things, you can keep the lifestyle you want.

Sources of Retirement Income

Diversifying how you earn money is key to a safe retirement. Besides Social Security, consider these options for your retirement income:

- Pensions: If your job offers a pension plan, check the details and benefits.

- Investment income: You can make money easily from stock dividends or bond interest.

- Rental income: Having rental properties can give you a steady income.

- Part-time work: Think about taking a part-time job during retirement for extra cash and to stay active.

- Look at all the ways you earn money.

- Consider how to add them to your retirement income plan.

Balancing Risk and Return in Retirement Income Plans

Finding the right balance between risk and return is very important for a retirement income plan. Investments can help your money grow. However, it’s also crucial to preserve your original amount. You must ensure that you have a steady income coming in.

- A mixed investment plan can lower risk.

- Spread your money across different types of assets.

- Consider how much risk you are comfortable with.

- Your investment timeline should also influence your plan.

Conclusion

In conclusion, making a budget and managing your retirement money is very important for a happy retirement. By knowing your expenses and adjusting your budget as needed, you can have a steady income when you finish working. It is key to balance risk and profit. You should also take care of your accounts and look for safe ways to earn money. Start planning for your retirement now to have a comfortable and stress-free future. Remember, you can begin saving for your future at any time. If you need help creating a retirement plan just for you, feel free to ask for expert advice.

Frequently Asked Questions

How much should I budget for retirement each month?

Your retirement budget will change depending on your situation. This depends on the lifestyle you want, your regular expenses, and your healthcare costs. A good place to start is to plan for 70-90% of what you spend each month before retirement. However, you should adjust this if your spending or income changes a lot. It could also help to talk with a financial advisor. They can assist you in creating a retirement budget that fits your financial goals.

What are the key factors to consider when budgeting for retirement?

Key factors for retirement budgeting include estimating living expenses, healthcare costs, inflation, desired lifestyle, emergency funds, debt management, and potential income sources like pensions or investments. It’s crucial to plan meticulously to ensure financial security during retirement years.

What are the best ways to reduce expenses in retirement?

There are several ways to save money when you retire. One way is to move to a smaller home. This can lower your housing costs, like rent or mortgage and property taxes. You can also spend less on things like travel and entertainment, which are discretionary expenses. Look for discounts for seniors. Check and compare prices for insurance and healthcare plans to find better rates. Lastly, if you have big family care costs, such as for a child’s wedding, make a plan for that. This will help you stick to your budget.

Important Disclosures:

This information is not intended to be a substitute for individualized legal advice. Please consult your legal advisor regarding your specific situation.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value, and may trade at prices above or below the ETF’s net asset value (NAV). Upon redemption, the value of fund shares may be worth more or less than their original cost. ETFs carry additional risks such as not being diversified, possible trading halts, and index tracking errors.

Fixed and Variable annuities are suitable for long-term investing, such as retirement investing. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Guarantees are based on the claims paying ability of the issuing company. Withdrawals made prior to age 59 ½ are subject to a 10% IRS penalty tax and surrender charges may apply. Variable annuities are subject to market risk and may lose value.

The principal value of a target fund is not guaranteed at any time, including at the target date.

Investments in real estate may be subject to a higher degree of market risk because of concentration in a specific industry, sector or geographical sector. Other risks can include, but are not limited to, declines in the value of real estate, potential illiquidity, risks related to general and economic conditions, stage of development, and defaults by borrower.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Stock investing includes risks, including fluctuating prices and loss of principal.

Investing includes risks, including fluctuating prices and loss of principal. No strategy assures success or protects against loss.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. To determine which strategies or investments may be suitable for you, consult the appropriate qualified professional prior to making a decision.

This material was prepared by Midstream Marketing.